.png)

Brief Discussion About Short Term Capital Gains Tax

Profit from the sale of a capital asset is known as capital gains.

A capital asset is a general term that refers to a variety of assets that produce income, including real estate, buildings, gold, equity investments, and other types of property.

Short-term capital gains and long-term capital gains are the other two divisions of capital gains.

Whether capital gains are long-term or short-term, they are taxed differently. Therefore to determine whether capital gains are taxable, they must be divided into short-term and long-term categories. In other words, the tax rates for long-term and short-term capital gains vary.

Let's learn more about short-term capital gains in-depth in this post.

What is Short Term Capital Gain (STCG)?

Any profit or gain that an individual receives from the sale of "short term capital assets" is referred to as a short term capital gain.

There are a few exceptions to this generalization, such as the fact that gains on depreciable assets are always subject to short-term capital gains tax.

Ramesh, for instance, spent Rs10 lakhs for a flat that he later sold for Rs 15 lakhs. He made a 5 lakh rupee profit. His short-term capital gain in this instance is Rs. 5 lakh.

What are Short Term Capital Assets?

Any asset that a taxpayer has possessed for less than or equal to 36 months following the date of first acquisition is considered a short-term capital asset.

- In light of the foregoing, it is crucial to keep in mind that the 12-month criterion has superseded the prior 36-month requirement for assets such as: Equity or preferred shares in a firm that is listed on a recognized stock exchange of India (listing of shares is not compulsory if the transfer of such shares has taken place on or before July 10, 2014).

- Securities that are listed on an established stock exchange in India, such as bonds, debentures, government securities, and so on.

- Units of UTI, whether or not they are quoted.

- Units of equity-oriented mutual funds, regardless of whether they are quoted.

- Bonds with no coupon, whether quoted or not.

It's also critical to remember that the 36-month requirement has been lowered to 24months for assets like:

- When it comes to shares of unlisted companies or immovable property like a piece of land, a structure, or both.

For instance, Ramesh bought a property on January 15, 2021, and sold it a year later, on January 12, 2022. Rajesh's apartment will be regarded in this case as a temporary capital asset.

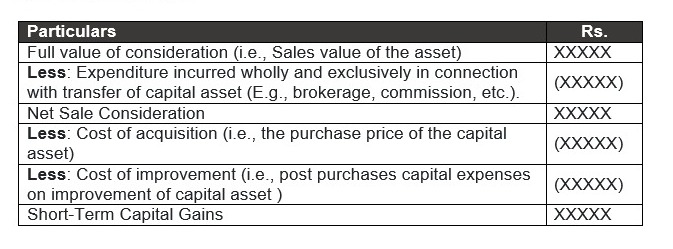

How is Short-Term Capital Gain Calculated?

The short-term capital gain on a transfer of a short-term capital asset is determined as follows:

For Example:

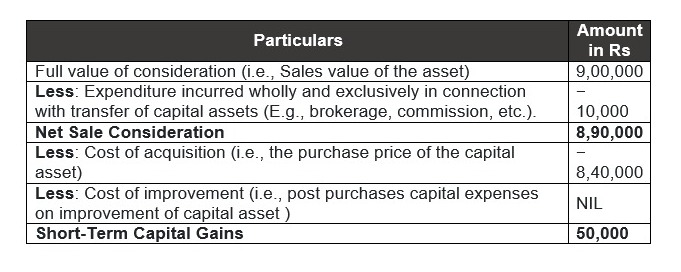

Mr. Rawat is a salaried employee. He bought gold in the amount of Rs.8,40,000 in December 2021, and he sold it for Rs.9,00,000 in August 2022. He paid Rs. 10,000 in commission when he sold the gold.

What is the amount of taxable capital gain?

Due to the fact that gold was bought in December 2021 and sold in August 2022 —i.e., after being held for less than 36 months—the gain is a short-term capital gain.

This is how the gain will be calculated:

What is Short Term Capital Gains Tax?

The India Income Tax Act, 1961 imposes taxes on gains or profits resulting from the transfer of short-term capital assets since they are viewed by an individual as "income" and as such are taxable. As a result, anyone who includes the proceeds from the sale of these assets in their taxable income in the year of the asset transfer is liable for the same amount of tax.

For the purpose of calculating the tax rate, short-term capital gains are divided into the following categories:

- Short-term capital gains covered under Section 111A.

- Short-term capital gains other than covered under Section 111A.

Examples of STCG Covered under Section 111A

The following are some examples of STCGs (Short Term Capital Gains) that are covered by Section 111A:

- STT-chargeable STCG resulting from the sale of equity shares listed on a reputable stock exchange (Securities Transaction Tax).

- When units of equity-oriented mutual funds are sold through are cognized stock exchange, STCG is assessed to STT.

- STCG resulting from the selling of units in a business trust

- STCG may occur on the sale of equity shares, units of an equity oriented mutual fund, or units of a business trust through are cognized stock exchange located in any International Financial Services Centre and consideration is paid or payable in foreign currency, even if the transaction is not subject to Securities Transaction Tax (STT).

Example of STCG not covered under Section 111A

The following are some examples of STCGs (Short Term Capital Gains) that Section 111A does not apply to.

- STCG due to equity share sales made outside of a recognized stock exchange.

- STCG resulting from non-equity share sales.

- STCG resulting from the sale of units in a mutual fund that is non-equity oriented (debt-oriented).

- The STCG applies to all government instruments, including bonds and debentures.

- STCG on the sale of non-share/unit assets, such as real estate and other movable property, as well as gold, silver, and other precious metals.

Short Term Capital Gains Tax Rates

The tax rate on STCG subject to Section 111A is 15%. (plus surcharge and cess as applicable).

The Standard slab rate, which is determined by the taxpayer's total taxable income, is applied to standard STCG, or STCG not covered by Section 111A.

How to Calculate Tax on STCG (Short Term Capital Gains)?

Let's use the following example to better understand how to calculate the tax that applies to STCG:

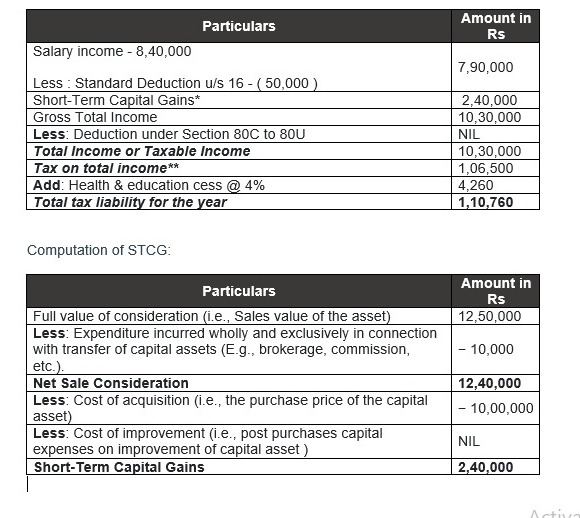

Mr. Soham (a resident of India and 40 years old) earns Rs.8,40,000 a year as a salaried employee at XYZ Ltd. He bought 10,000 equity shares in ABC Ltd. in December 2021 for Rs.100 per share and sold them in April 2022 for Rs.125 per share(brokerage Re.1 per share). Mr. Soham paid the securities transaction tax and sold the shares on the Bombay Stock Exchange.

What will be the tax liability of Mr. Soham?

To determine Mr. Soham's tax liability, we must first determine his taxable income. The Following formula will be used to calculate taxable income:

STCG is subject to tax at a rate of 15% because it falls under section 111A.

Salaries are taxed at the standard rate since they are regarded as regular income. The standard tax rates for residents under the age of 60 for the financial year2021–2022 are as follows:

- Nil up to income of Rs.2,50,000

- 5% for income above Rs.2,50,000 but up to Rs.5,00,000

- 20% for income above Rs.5,00,000 but up to Rs.10,00,000

- 30% for income above Rs.10,00,000.

In addition to the aforementioned, a 4 percent education and health cess will be applied to the taxable amount

STCG is adjusted in relation to the baseline exemption limit.

The basic exemption threshold is the amount of money over which someone is exempt from paying any taxes. The basic exemption limit that is applicable in the case of a person for the financial year 2021–2022 is as follows:

- Residents 80 years of age or above are eligible for an exemption up to Rs5,00,000.

- The exemption threshold for citizens who are 60 years of age or older but are under 80 is Rs3,00,000.

- For residents under the age of 60, the exemption threshold is Rs2,50,000.

- No matter their age, non-residents are only exempt up to a maximum of Rs2,50,000.

- AHUF (Hindu Undivided Family) is only eligible for an exemption up to Rs.2,50,000.

Points to be noted

- If your entire income, including STCG, is less than Rs2.5 lakhs after any necessary tax deductions, your total tax burden is zero, and there is also no obligation under Section 111A because deductions are permitted up to the basic tax exemption amount.

- However, a flat 15 percent STCG tax would be applied if your total income, including STCG, exceeds Rs2.5 lakhs. (However, if total income is less than 5 lakhs, a rebate under Section 87a will be available, covering up to Rs12,500 of tax due under the current income tax system.)

Deductions under Section 80C to 80U and STCG

Under Sections 80Cthrough 80U, short-term capital gains, as those terms are defined in Section111A, are not deductible. However, such deductions can be claimed from STCG in addition to those allowed by Section 111A.

Conclusion

The taxes that will be applied on gains should be considered by people who intend to invest in short-term capital assets. Any loss incurred due to the sale or transfer of one short-term capital asset may be offset (adjusted) by any gain realized due to the sale or transfer of another short-term capital asset. The most crucial point to keep in mind is that both short-term capital gains (STCG) and long-term capital gains can be offset by short-term capital losses (STCL)(LTCG). Taxpayers should be aware that this loss cannot be adjusted against any other income despite the foregoing.

About Jordensky

At Jordensky, we are committed to providing an experience of the highest caliber while specializing in accounting, taxes, MIS, and CFO services for startups and expanding businesses.

When you work with Jordensky, you get a team of finance experts who take the finance work off your plate– ”so you can focus on your business

.png)