There are 8 important steps of the accounting cycle that is very essential for businesses to keep a perfect financial record and make sure compliance with regulatory standards. The Accounting Cycle Steps contains eight steps, beginning with identifying transactions and ending with closing the books. The importance of accounting for businesses helps in tracking the income and expenses, making informed financial decisions, and preparing for audits. Moreover, make sure that all financial activities systematically recorded, analysed, and reported.

What Is the Accounting Cycle?

A systematic process that helps to identifying and recording the transactions and ends with closing the books for a period is accounting cycle. We provide the best services in accounting services in Bangalore that helps to handle accounting tasks efficiently. The accounting cycle steps helps to handle the every transaction accurately tracked and reported, which is essential for maintaining all the financial records and compliance.

Purpose of the Accounting Cycle

The primary purpose of the accounting cycle is to create accurate financial statements that is for both the internal use by the management and external use by stakeholders. This accounting cycle is very important for businesses; We provide help to manage tax obligations effectively with our accounting services in Pune all you have to follow the 8 steps of the accounting cycle that promises to keep the financial data is up-to date and accurate, which leads to the perfect strategic planning and decision-making.

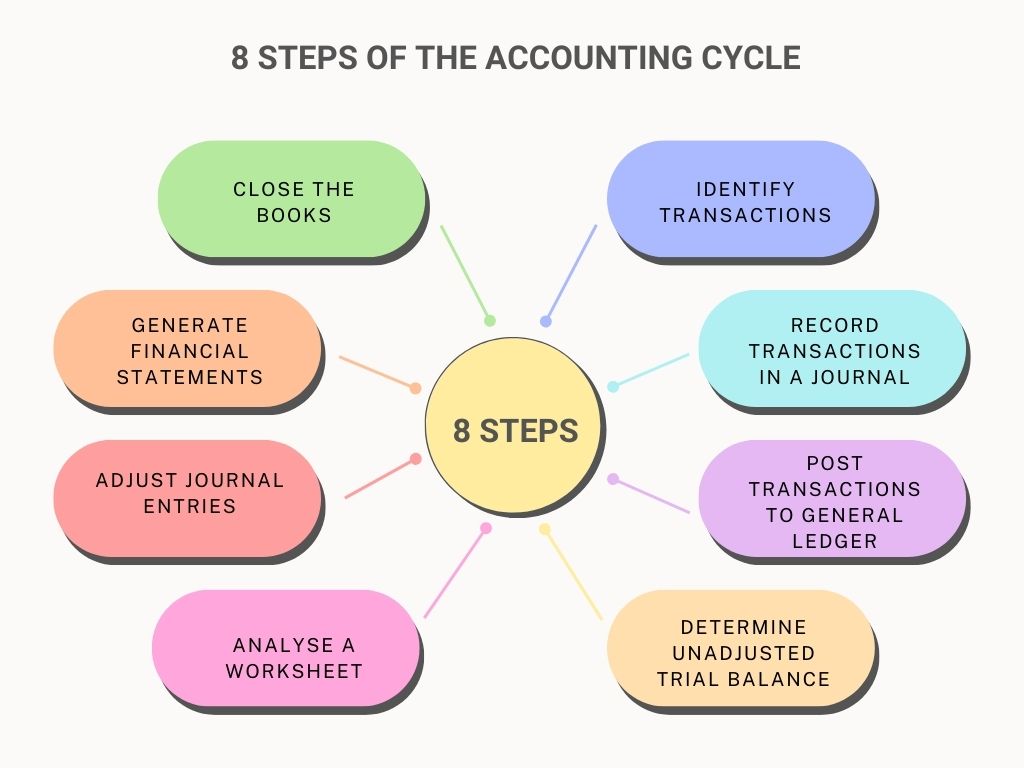

8 Steps of the Accounting Cycle

The accounting cycle has 8 steps that is designed to keep the financial records accurate and up-to-date. These steps provides a solid approach to tracking and managing financial transactions throughout the accounting period.

1. Identify transactions

The first very step in the accounting cycle is to identify and analyse all transactions that affect the business. It includes sales, purchases, receipts, and payments. We help you to identify the transactions and suggest for necessary decisions.

2. Record transactions in a journal

After the identification of transactions, we have to record everything in a journal in chronological order. This step helps to keep documenting the details of each transaction, including dates, amounts, and accounts affected, providing a clear and organized record of financial activity.

3. Post transactions to general ledger

Post these data to the general ledger that consolidates all the financial information, categorizing it into individual accounts, which helps in summarizing the financial status of the business.

4. Determine unadjusted trial balance

The unadjusted trial balance is listing all accounts and their balances from the general ledger. This step helps to get the total debits equal total credits and provide a preliminary check for any errors before adjustments made.

5. Analyse a worksheet

Analysing a worksheet is an optional task but it is very useful step, which involves organizing and reviewing unadjusted trial balance figures. Also helps to identifying any necessary adjustments and ensures that the financial statements will be accurate.

6. Adjust journal entries

Adjusting journal entries is helps to account for accrued and deferred items that have not yet been recorded. This step makes the revenues and expenses recognized in the period in which they occur, maintaining the accuracy of financial statements.

7. Generate financial statements

Businesses generate financial statements, which including the income statement, balance sheet, and cash flow statement. These documents provide a detailed overview of financial performance and the position of our company.

8. Close the books

Close the books is the final step that involves zeroing out temporary accounts that is revenues and expenses and transferring the balances to permanent accounts such as retained earnings. This helps and prepares the accounts for the next accounting period and finalizes the financial records of current period.

Conclusion

In an accounting cycle there are 8 steps of the accounting cycle that is important for maintaining a solid and reliable financial records. The audit and accounts services in Mumbai perfectly utilizing the benefit of accounting services from a very structured approach to managing the financial tasks. Following by these Accounting Cycle Steps you can makecompliance and informed decision-making. Moreover, it helps companies to achieve financial clarity and reduce mistakes for any financial scrutiny.